A smarter starting point for buying a car

- Published On

- April 20, 2026

- Category

Thinking about buying a car but not sure where to start? You are not alone. For most people, it starts the same way: scrolling through listings, comparing prices, and trying to figure out what looks like a good deal. But the most important part of smart car shopping does not happen when you find a vehicle. It happens before you even start looking.

At OMVIC, we regularly hear from buyers who realize too late that they cannot afford the monthly payments they agreed to. By the time that happens, the contract is signed, which can make resolving the issue more challenging. In some cases, people miss payments, damage their credit, and end up dealing with financial stress that affects much more than just the car.

That is why the smartest place to start is not with a vehicle. It is with your budget.

Car Affordability Is Getting Riskier

Missed Payments Are Rising

The situation many buyers do not expect

Think about this: you find a car that seems perfect. The price looks reasonable and the monthly payment sounds manageable. You sign the paperwork, drive it home, and everything feels exciting at first.

Then the real costs start to show up.

Insurance ends up costing more than expected. Gas adds up quickly. Then a repair comes along. Suddenly, a payment that once felt manageable becomes overwhelming. It’s a situation OMVIC hears about again and again.

Once you’ve signed the contract, you’re legally responsible for those payments. According to the Financial Post (December 2025), nearly 2% of Canadian car owners are already falling behind, and that number is rising. Canadians across all age groups, from first-time buyers to seniors, are increasingly struggling to keep up, making it more important than ever to set a realistic budget before you buy.

The three questions every buyer should answer first

Before you even start browsing listings, there are three questions that matter more than anything else.

1. What can I realistically afford?

This isn’t just about the price of the vehicle. It’s about your real financial situation, including your income, savings, monthly bills, and how much flexibility you actually have in your budget.

Many buyers focus on what they want to afford rather than what they can afford. Starting with OMVIC helps you understand the difference and avoid committing to something that could create long-term financial stress. Visit OMVIC’s car-buying tips page to learn more about buying and financing options.

Most major Canadian banks have a car loan calculator that can be used before you begin looking at cars. These calculators are really helpful in determining what you can realistically afford to pay monthly for a vehicle.

Young Buyers Hit Hardest

Percentage of buyers who missed 3+ payments

Younger Buyers

2.94%

2.54%

Seniors

1.33%

1.03%

2. What is the full monthly payment?

Your monthly payment is more than just the loan amount. It includes:

- The loan payment itself

- Insurance

- Fuel

- Maintenance and repairs

- Registration and taxes

- Parking (for many buyers)

Once all of these costs are added together, the true monthly amount is often much higher than people expect. That’s why using budgeting tools before you start shopping is so important; they help you understand what owning that vehicle will really cost every month, not just what it looks like on paper.

The CAA driving costs calculator takes all of these factors into account and provides a more realistic estimate of the full cost of owning or leasing a vehicle.

Understanding the full cost of ownership before you shop helps you avoid surprises later and helps ensure the car you choose fits your life, not just your wish list.

3. What will my loan actually look like?

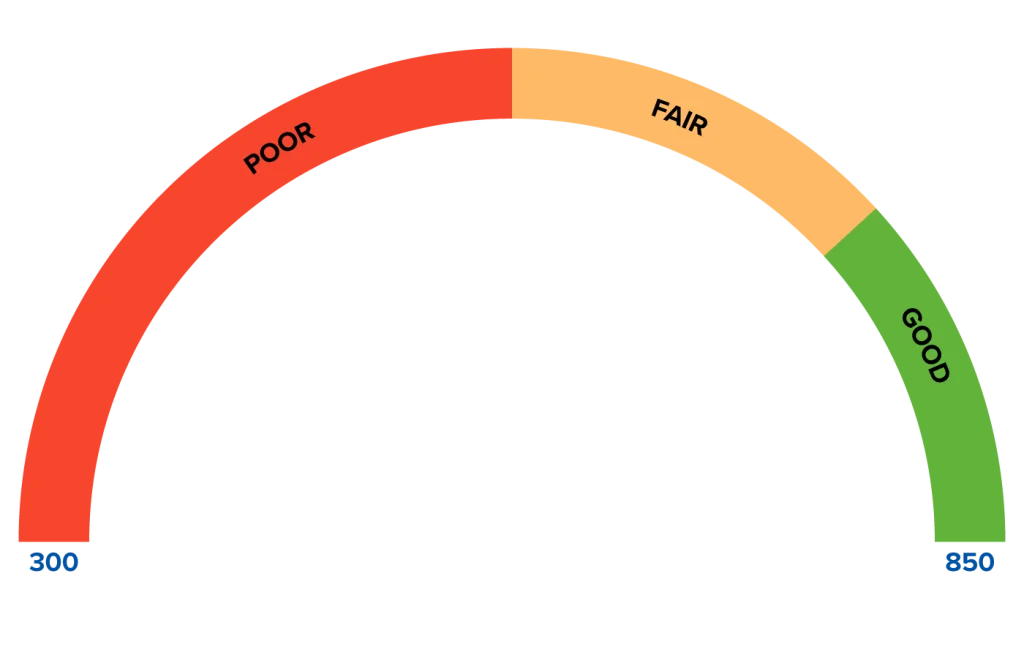

Another step many people skip is checking their credit score before they start looking at cars. Your credit score helps lenders decide what interest rate you will be offered, and that has a direct impact on your monthly payment. If your score is lower, the payment can be much higher than you expect.

Your credit score is simply a number that shows lenders how risky it might be to lend you money. In Canada, it is created by two credit bureaus: Equifax and TransUnion. The higher your score, the easier it usually is to get a loan and the less you will pay in interest.

In simple terms:

In simple terms:

- 660 and above is considered good

- 300–559 is considered poor

- Anything in between is considered fair

If your score is below the good range, it may be harder to qualify for a regular car loan from a bank or credit union. That could mean higher interest rates and higher monthly payments, which can make the car much more expensive than you expected. Since October 2025, the average car loan interest rate has ranged between 6.5%-8%, according to Stats Canada.

That is why it is so important to check your credit before you start shopping and compare more than one loan option before you agree to anything. A few extra questions at the beginning can make a big difference in what you end up paying every month.

For first-time buyers or newcomers who do not yet have a credit history, major banks such as RBC, Scotia Bank and TD offer newcomer and first-time buyer programs. These programs may look at employment stability instead of just credit history, but it is still important to compare options and make sure the payment is realistic for you.

Start with your budget, not the vehicle

The biggest mistake many buyers make is starting with the car instead of starting with their finances. By the time they realize the payments are too high, they’re already committed.

By starting with OMVIC, you get the tools and guidance to help you understand the full cost of your purchase so you can set a realistic budget, compare options confidently, and avoid financial surprises down the road. Smart car shopping starts with OMVIC. Do your research first, it could save you a lot of money and stress.